Standard Chartered Plc V Guaranty Nominees Limited and Others [2024] EWHC 2605 (COMM) (15 October 2024)

- This recent decision of the English High Court sheds light on the construction and proper interpretation of the fallback provisions relating to interest rate benchmarks contained in an offering circular of preference shares issued by a bank.

- Preference shares typically entitle investors to receive a fixed dividend (payable at the board’s discretion) and allow their holders to rank in priority over the ordinary shareholders of a company as to the return of capital on a winding up, effectively constituting a peculiar class of shares.

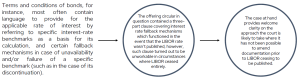

- Dividends on the concerned preference shares were payable at a fixed rate of interest, turning then into a floating rate equal to 1.51% plus Three Month “LIBOR”, that is, the London Interbank Offered Rate benchmark.

The potential of interest rate benchmarks to undermine market stability and distort the real economy are now widely acknowledged and regulated at global level. For this reason, the decision is likely to be of wider interest to the finance community, given that provisions dealing with the selection and application of interest-rate benchmarks are commonly found in various types of financial contracts, especially where these are governed by English law, as is often the case with debt securities of several Italian and European issuers, meaning also that such contractual documentation would be subject to English law principles of contractual construction and interpretation.

While the claimant bank submitted that a term should be implied into the third fallback provision to refer to the “reasonable alternative rate” as the applicable rate of interest; on the other, the

defendant investment fund submitted that the term to be implied was, instead, that the preference shares should be redeemed.

The court ruled that:

- there had to be a term implied into the contract to address the cessation of LIBOR given that the fallbacks expressly included in the contract were not workable as the preference

shares would not be commercially or practically coherent without implying such term, and - the term to be implied in such a case would refer to the “reasonable alternative rate” of interest.

The court then looked at what the meaning of “reasonable alternative rate” should be:

- To provide a workable definition of “reasonable alternative rate” in line with the principle of business efficacy, the court considered various factors, including the criteria of the regulators in proposing an alternative rate, such as resilience, as well as market practice, and the intention of the parties as inferred from the contract.

- The court also pointed out that the inclusion of a fallback clause in the offering circular was evidence that the parties did not want issues relating to LIBOR publication to frustrate the contract in the first place.

Conclusions

The bottom line is: interest rate fallback mechanisms should be very clearly documented, by referring to specific standards and/or unambiguous sources of information (such as the opinion of a specific entity) in order to address any potential uncertainty in the determination of the interest rate. The use of language that is as simple and comprehensible as possible is key.

The full judgement is available at:

https://www.judiciary.uk/wp-content/uploads/2024/10/FL-2024-000005-Standard-Chartered-Plc-v-Guaranty-Nominees-Limited-and-Ors-15.45.pdf

The press summary is available at:

https://www.judiciary.uk/wp-content/uploads/2024/10/Press-Summary-LIBOR-Judgment-Summary-Standard-Chartered-PLC-v-Guaranty-Nominees-Limited-2024-EWHC-2605-Comm.pdf

Flash news by Bianca Casini – bianca.casini@crccdlex.com