What is the focus of this alert?

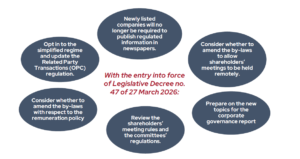

Legislative Decree no. 47, approved on 27 March 2026.

Who is this alert targeted at?

General counsels, legal offices, corporate secretary offices, secretaries of the board of directors, CFOs, and listed companies’ investor relators.

What is the purpose of this alert?

To identify the key changes introduced by the reform of the Consolidated Financial Act and of the Italian Civil Code.

Consolidated Financial Act. The main thematic areas covered

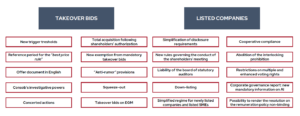

Key changes – takeover bid

New trigger thresholds

Full takeover bid: (i) single threshold of 30% of shareholding or voting rights; (ii) elimination of the reduced threshold of 25% for larger companies (non-SMEs) and of the possibility for SMEs to identify a threshold ranging between 25% and 40% in their by-laws.

Consolidating takeover bid: threshold raised from 5% to 10%.

Exemptive voluntary takeover bid: threshold lowered from 60% to 50%.

Reference period for the “best price rule”

The reference period for assessing purchases made prior to a takeover bid in order to determine the minimum bid price has been reduced from 12 to 6 months. For an exemptive voluntary takeover bid, the reference period for assessing any subsequent mandatory takeover bid has also been reduced from 12 to 6 months.

Offer document in English

Introduction of the possibility to draft the offer document in English (or in another language commonly used in the financial market). In such cases, a summary note in Italian is required.

Consob’s investigative powers

Consob’s power to suspend proceedings will no longer arise whenever “additional information” is required, but only when there is “serious lack of information”. When authorisations by sector-specific regulations are needed (e.g. by the Bank of Italy, the ECB, or IVASS), the deadline for Consob’s approval is extended from 5 to 10 days from the date of the notification of such authorisations.

Acting in concert

The definition of persons acting in concert is amended. Concerted action aimed at maintaining control is no longer relevant.

The absolute presumption of concerted action becomes a rebuttable presumption (thus allowing for evidence to the contrary).

Full acquisition upon shareholders’ authorization

Introduction of a new procedure, which allows the extraordinary shareholders’ meeting of listed companies to resolve upon the acquisition of the company’s entire share capital by a party identified by the board of directors, with the favorable vote of at least 75% of the share capital represented at the meeting. The shareholders’ meeting’s resolution also requires the favorable vote of the majority of the issuer’s shareholders present at the meeting, excluding: (i) the shareholder who submitted the proposal and those acting in concert with that shareholder, as well as (ii) shareholders who, individually or in concert, hold a majority stake—even if a relative majority—provided it exceeds 10% of the company’s share capital.

Squeeze-out

Extension of the squeeze-out mechanism beyond full takeover bids to cover also sell-out scenarios (i.e., purchases pursuant to Article 108(2) of the TUF). The reform broadens the application of the squeeze-out following a full takeover bid to financial instruments other than shares (e.g., savings shares).

Lowering of the squeeze-out threshold from 95% to 90%.

Anti-rumour provision

Introduction of a so-called “put up or shut up” rule (of anglo-saxon origin), aimed at reducing circumstances od uncertainty and preventing unwarranted speculations. Where rumors or market speculations are spreading, Consob may set a deadline by which a potential offeror must publicly announce whether it intends to launch a takeover bid. In the event of no response or a negative statement, the potential offeror will be prohibited from launching an offer (in respect of any financial instruments of the same issuer) for the following 12 months.

New exemption from mandatory takeover bid

The reform expressly provides that Consob may, by regulation, identify a new exemption from the mandatory takeover bid requirement in the event of a threshold being exceeded as a result of capital contributions in kind, in a manner analogous to the exemptions already provided in cases of mergers and/or demergers.

Takeover bid on EGM

Introduction of a provision granting Borsa Italiana, as the market operator, the authority to adopt measures in line with those under Article 110 of the TUF (such as suspension of voting rights and the obligation to sell shareholdings), as well as other appropriate measures.

Key changes – listed companies

Simplification of disclosure requirements for newly listed companies

An exemption from the obligation to publish regulated information in newspapers

for newly listed companies that have opted, through a statutory amendment, for the simplified regime, resulting in reduced costs and compliance obligations.

Shareholders’ meetings

Remote participation is encouraged (unless requested by shareholders representing at least 1/20 of the share capital with voting rights on the items on the agenda); in the absence of an express statutory provision, the board of directors may decide on the relevant matter.

Provisions have also been introduced to limit “merely disruptive” activities.

Liability of the Board of Statutory Auditors

For listed companies, the limitation of liability provided under Article 2407 of the Italian Civil Code is excluded.

Down-listing

Provision for an alternative to delisting: the transfer from the regulated market Euronext Milan to the multilateral trading system Euronext Growth Milan – EGM, resulting in reduced compliance obligations and costs.

Simplified Regime

Introduction of a simplified regime for newly listed companies and listed SMEs with a market capitalization of less than 1 billion.

The companies must opt in, with an amendment to their by-laws which can provide for: (i) more flexibility for transactions with related parties, (ii) corporate bodies to be appointed using methods other than list voting, (iii) exclusion of certain grounds for the exercise of withdrawal rights, and (iv) simplified quorum for the approval of the amendments to the by-laws.

Cooperative compliance

Operators are permitted to submit questions to Consob and the Bank of Italy for a preliminary assessment of specific situations that could result in violations of the provisions subject to their respective oversight.

Abolition of the interlocking prohibition

The prohibition preventing senior officers and individuals holding positions on management, supervisory, or control bodies of companies or groups operating in the banking, insurance, and financial markets from assuming or exercising equivalent positions in competing companies or groups has been abolished.

Restrictions on multiple and enhanced voting rights

Multiple and enhanced voting rights are neutralized for resolutions concerning: (i) mergers that result in delisting; (ii) transfer of the registered office abroad; (iii) total acquisition following shareholders’ authorization; (iv) delisting; (v) down-listing.

Corporate governance report: new mandatory information on AI

New disclosure obligations have been added concerning the company’s policies, if any, regarding (i) the use and monitoring of new technologies, in particular AI systems, within administrative, organizational, and accounting structures; and (ii) the management and monitoring of IT risks, including cybersecurity risks and risks arising from the integration of new technologies into administrative, organizational, and accounting structures.

Possibility to render the resolution on the remuneration policy non-binding

The by-laws can be amended to set forth that the shareholders’ approval of the remuenration policy is not binding. If the by-laws is not amended, the shareholders’ resolution remains binding.

Listed companies: what’s next?

Italian Civil Code. Main thematic areas covered

- Reorganization of governance systems

- Appointment of the chairman of the board of directors

- Conflict of interest

- Corporate information

- Non-delegable powers

- Non-compete obligation for general managers

Key changes – corporate governance

Reorganization of Governance Systems

Reorganization and equal treatment of the three governance systems provided for by the Italian Civil Code. The so-called traditional system is no longer considered the default model. The by-laws of each company must specify the system adopted, choosing between a model with a board of statutory auditors (traditional), a supervisory board (dualistic), or a management control committee (monistic).

Corporate Information

Non-executive directors are not jointly and severally liable if, in making their decisions, they reasonably rely, including in light of their specific expertise, on information received in accordance with the law and the by-laws.

Appointment of the chairman of the board of directors

The directors appoint the chairman of the board of directors, if not appointed by the competent body, unless otherwise provided for in the by-laws.

Non-delegable powers

Decisions regarding access to crisis and insolvency resolution frameworks, including decisions concerning the determination of the content of the proposal and the terms of the plan, are expressly defined as non-delegable by the board of directors.

Conflict of interest

Where a director has an interest in a given transaction, the by-laws or the board of directors, through its internal regulations, may establish conditions, procedures, and additional limitations on such director’s participation in board meetings.

Non-compete obligation for general managers

An explicit non-compete obligation is introduced for general managers, which may be waived with the company’s authorization, as well as an express prohibition on using, for their own benefit or that of third parties, information acquired in the course of their duties.

Flash news by:

Michele Crisostomo – Michele.Crisostomo@crccdlex.com

Guido Masini – Guido.Masini@crccdlex.com

Guido Bartolomei – Guido.Bartolomei@crccdlex.com

Nicola Caielli – Nicola.Caielli@crccdlex.com

Valentina Dragoni – Valentina.Dragoni@crccdlex.com

Fiona Chung – Fiona.Chung@crccdlex.com

Marco Renzi – Marco.Renzi@crccdlex.com

Ilaria Alessandroni – Marco.Renzi@crccdlex.com

Giuliano Tullio – Guliano.Tullio@crccdlex.com